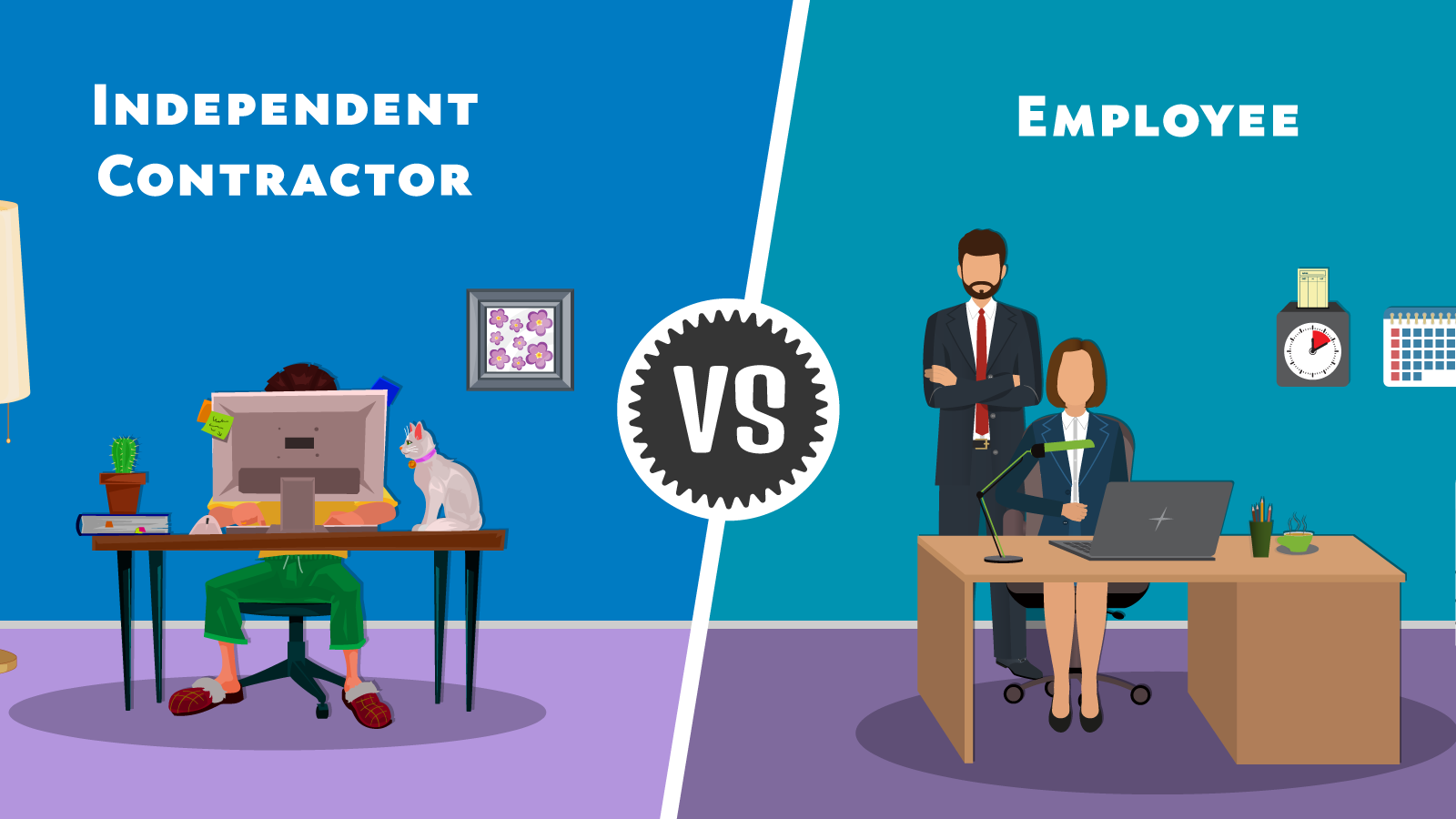

Independent Contractor or Employee: How Do I Know?

Jason Levan

/

November 11, 2021

The easy answer is, there is no easy answer.

Even Janice Fritz, an HR consultant for Kuzneski Insurance Group, still struggles with these decisions.

“There’s a lot of things to consider, and it’s not easy. Even though I’ve been in HR for over 20 years, it’s still kind of a gut feeling,” Janice admits.

“It’s not an easy question to answer because there’s no bright line, black or white. I always say that recruiting is an art, not a science,” she says. “It’s kind of the same way with who is an independent contractor. It’s a totality of the circumstances. That’s as much guidance as you have.”

Several factors go into the decision to classify a worker as an independent contractor (IRS Form 1099) or as a payrolled employee (IRS Form W-2). Yet, it is an important determination, because misclassification can trigger costly financial penalties.

So, what’s the difference?

It boils down to this: The IRS looks at three general categories to determine whether a worker is a contractor or an employee: behavioral, financial and relationship.

- Behavioral: Do you control (or have the right to control) what the worker does and how they do their job?

- Financial: Are the business aspects of the worker’s job controlled by the payer, such as how the worker is paid, whether expenses are reimbursed and who provides the supplies?

- Relationship: Are there written contracts or employee-type benefits (insurance, 401(k), vacation, etc.)? Is the relationship permanent? Is the work that is performed a key aspect of the business?

In general, if the employer has a say over what the worker does, dictates the financial business aspects and provides benefits, then the worker is probably a W-2 employee. A worker is usually a 1099 employee if they get to determine how to do their job, are financially responsible for expenses and do not receive benefits. Independent contractors typically don’t have a long-term relationship with a company.

For example, an employee:

- Does not own their own business

- Is paid hourly, a salary or by piece

- Uses an employer’s materials, tools, equipment

- Typically works for one employer

- Has a continuing relationship with the employer

- Performs work assigned by the employer

And an independent contractor:

- Runs their own business

- Is paid upon completion of a project

- Provides own materials, tools, equipment

- Works with multiple clients

- Has a temporary relationship with employer

- Decides when/how to do the work

Luckily, the IRS does offer some help, Fritz says. In 2020, the IRS replaced the 20-Factor Test, long considered the standard for evaluating this decision, with the more voluminous Publication 15-A. (The former is still a useful tool though, as far as Janice is concerned.)

“If you can put yourself in the IRS’s shoes and make a call, that’s one way to do it,” she says.

And remember, KIG HR advisors, like Janice, for instance, can help guide your decision. Give us a call at (724) 349-1919.

For more information, read these blogs as well:

How Do Worker Classifications Affect My Business?

Contractor or Employee: Tax Forms You'll Need

What If I Misclassify a Worker?

Share Your Thoughts